The cost of debt… it sounds like a philosophical question or an attention-grabbing headline on the detrimental cost to society of Millennials living their lives on credit cards and buying too much avocado toast. What I simply mean is “what does it cost to borrow money”? You can borrow money for a variety of reasons however I am referring specifically in this article to borrowing to buy a property, aka getting a mortgage, and how cheap debt pushes property prices up.

If you speak to your bank, a mortgage broker or even type into google “mortgage rate” you’ll be inundated with offerings hovering around 1.8 to 2.2% (October 2021). These are annual percentage rates and simply put, if you had a mortgage rate of 2% you would be paying $20,000 per year on a $1million loan. But where does this magical 2% rate come from and is that high or low?

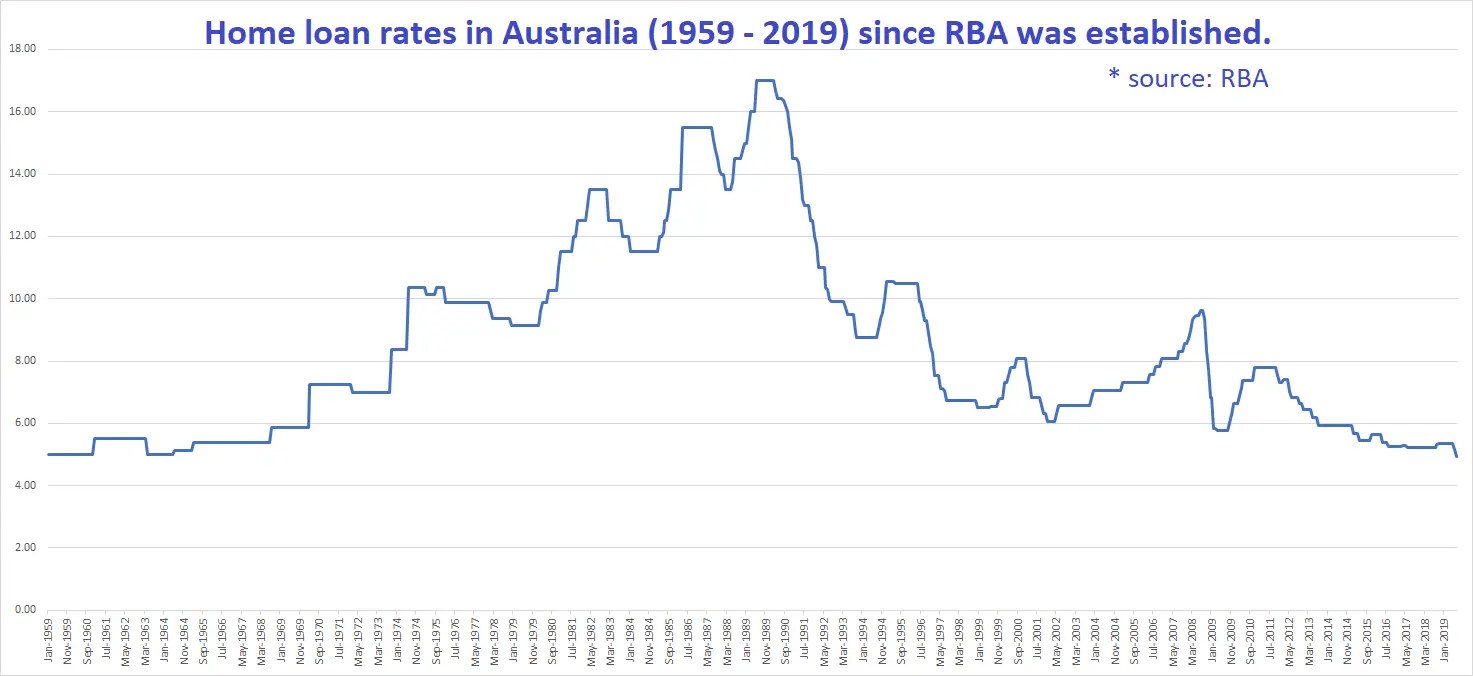

To answer the last question first, current mortgage rates are the lowest they’ve ever been. In January 1990 you could have been paying 17% for your mortgage and rates have never really been lower than 5 or 6% even during the Global Financial Crisis in 2008. So, why and how are mortgage rates so low right now? Which leads me back to the first question of how is the rate set?

All interest rates, whether earned on money deposited in a savings account or conversely paid on money borrowed to buy a house, are set off the Reserve Bank of Australia’s (RBA’s) cash rate plus a number of other factors (see previous post here). The RBA announces the new cash rate on the first Tuesday of every month (except January) and weighs a number of economic factors such as unemployment and inflation to determine the rate. The RBA can use the cash rate to influence borrowing or saving to help stabilise the economy.

Currently the RBA cash rate is 0.10%, the lowest it has ever been and almost zero.

If the RBA wants to encourage borrowing the cash rate will be lowered (you pay less interest) and if they want to encourage saving the cash rate will be increased (you earn more interest). Put another way, if the RBA wants people to borrow more they will make it cheaper and easier to do so. But why would the RBA want people to take on more debt?

During the global Covid pandemic with millions of people dying worldwide, billions being locked down for extended periods of time and countless businesses having to temporarily close and potentially going bust, the hit to the global economy has been huge. The Australian economy has been affected by Covid in many ways.

The total unemployment rate has drastically increased from 5.1% just before Covid hit in Feb 2020 to 7.4% in July 2020.

Furthermore, inflation has gone from around 0% annual inflation in the year ending 2019 to almost 4% in 2020. An increase in inflation is generally a good thing but means the cost of living has increased and the rate at which it has increased during this time is significant. So, less people are employed and it costs more to live. Because of this and many other factors, the RBA is trying to stimulate the economy to spend. And the more we spend the more we borrow.

Therefore, currently you could say the cost of debt is cheap. It does not cost as much as it has done historically (or ever!) to borrow money, and because it is cheap, we can borrow more. For instance, in 2014 the average interest rate was 6%, which on a $1million loan would cost you $60,000 per year. Lending institutions calculate your loan size based on income, current spending habits and a number of other factors. If none of these factors have changed but the interest rate has dropped, because you used to be able to afford $60,000 p.a. on $1million but now it only costs $20,000, the bank is happy to lend you more because you can service a higher level of debt on a lower rate.

And this finally leads me to explain how being able to borrow more money means that buyers can pay more when buying property, which is driving property prices up. If you could only borrow $1million before and a house at auction goes past this point you would have been out. But now you can borrow $1.2million you still have more spending power to stay in the auction. It doesn’t really matter what the property is worth (up to a certain perceived value point), if there are two or more interested buyers with money to spend still interested in buying the property, the price will be set just higher than the lowest bidder’s limit.

The RBA and the government do not want to create a property bubble, nor push prices up any further but these unprecedented times cause for drastic action. Which takes me back to the Millennials at the start of this article and the economic conundrum of housing affordability for the younger generations. Should they stop eating avocado toast and save more, or should the government intervene with drastic changes to the property industry (via duties, taxes, incentives and disincentives)? Or will it be left up to the mums and dads to personally redistribute generational wealth?