While I have been battling the sleepless minefield of having a newborn and a toddler my poor husband has been in London for his new job. While it seems he should be having the best time sans wife and kids (and of course he has been enjoying himself, not least of which includes attending the Aust v Wales Rugby World Cup match!), he has had to find us a rental house. And wow it seems the London property rental market is tough!

You can start by looking at the online property websites (similar to domain.com and realestate.com in Australia) http://www.zoopla.co.uk and http://www.rightmove.co.uk. But as we discovered, a lot of the properties listed have already been rented, a lot of the properties don’t even get listed on these sites, and if the property is any good, won’t even have time to be listed. The best advice we got was to register interest with the good real estate agents in the areas you wish to rent. Then they have met you, know your story, have a personal connection with you, and when a property that fits your criteria becomes available, they can call you to discuss.

You have to figure out where you want to live. Luckily my husband and I have both lived in London, so know some areas really well. We also asked friends for recommendations for good “family” areas in London, because we sure didn’t take notice of those in our 20s! And then we had the debate whether we live in London (borough) or Greater London (in the other 31 boroughs extending to Twickenham, Croydon etc). We decided if we were moving to London, we wanted to live in London and we would forgo space and a backyard for proximity!

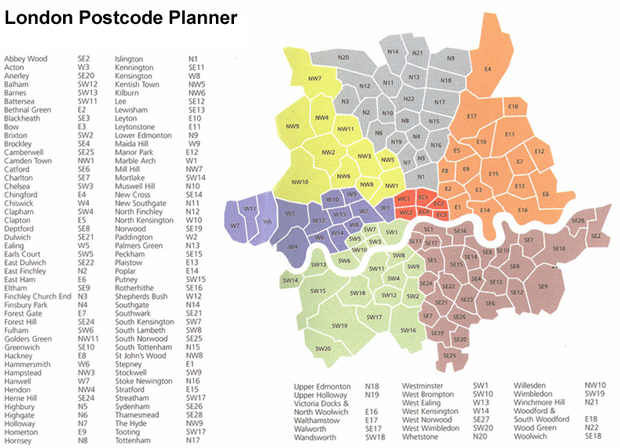

Understanding the postcodes in London may seem daunting at first but is really easy. Postcodes start with a compass location; North, South, East and West, and are then followed by a number indicating proximity to the centre. Postcodes centre on the “City of London”, officially Charing Cross Station (WC1). The central postcodes are given a “C” reference and are only East (“EC”) and West (“WC”). You then move out from these central postcodes to postcodes starting with simply “N” for north, “NW” for northwest, “S”, “SW” “E”, and “W”. An example being N1 for Islington, which is north of the City of London and very close, to SW20 for West Wimbledon, which is southwest of the City of London and the furthest postcode before you move out of the London borough .

Geeking out here, UK postcodes are brilliant because with just the street number and the full postcode, you can find an exact location in the whole of the UK. A full UK postcode will firstly identify which area in the whole of the UK (not just London) and then the street and even the side of the street. So for example “SW1 2AA” tells me SW1 is Victoria/Westminster and 2AA is Downing Street. So if I add the number 10 I will find my way to David Cameron’s house. Love it!

Most importantly you really need to work out your budget. The research I did suggested London rents can cost 30-50% of your net income. Apparently some credit agencies will advise landlords against leasing to tenants where the rent is greater than 30% of gross income. I thought this sounded quite high and we would pay nowhere near that much, but on one income (until I return to work next year) and needing 3 bedrooms, we are definitely pushing our upper limit. Then you have to factor in those unexpected UK charges of TV Licence fees (what the?!) and Council Tax (equivalent of Council Rates, paid by the landlord in Australia), and of course transport charges depending on which zone you live in.

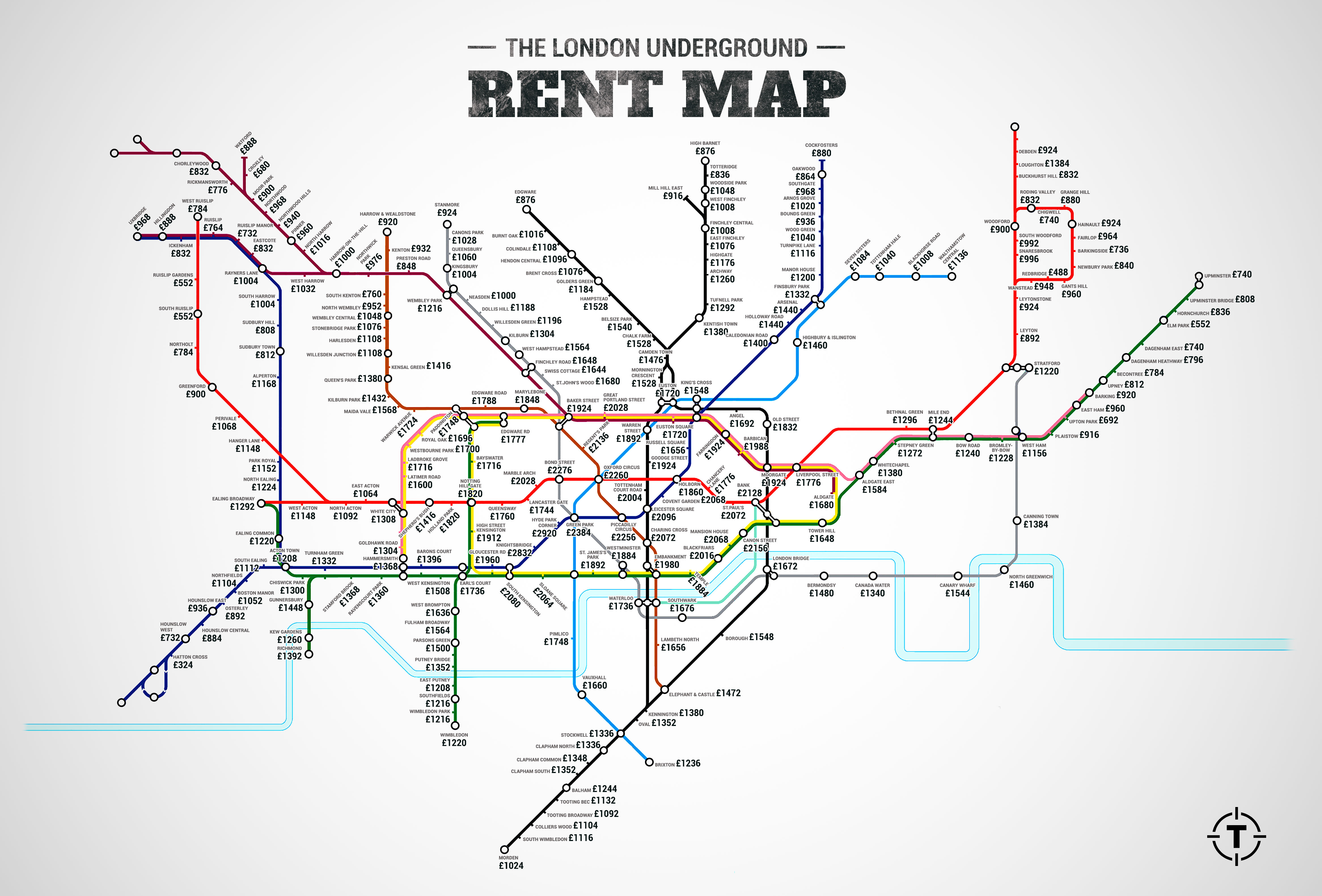

This picture shows a great comparison of the rental costs in London. I’m not sure if the amounts are current but if you’re comparing areas, this is pretty spot on!

Then be prepared for the competition! The rental market is fierce and prospective tenants regularly offer more rent in order to secure a property, and good properties often get leased within days. So you have to be all over it like a fat kid on a cake, and be prepared to pay up for a property you really love.

Because we now have kids and things such as health and wellbeing now rank so much higher than where the best pub is, I wanted to understand where one lives in London in relation to levels of pollution. Luckily I have a cousin who is a Paediatric Allergist in London and she simply advised against living on main streets, suggesting even just one street back from a main street has no more pollution than the next big city.

So take the time to understand the areas in which you want to live. Spend a Sunday walking these areas and discovering on which streets you’d like to live. Especially work out how close your nearest underground or overland station is, and how you get to work and other regular haunts.

And finally, the best advice I got when moving over in 2006, which is still relevant, was to live where you friends live. Even though the transport system in London, while sometimes unreliable, is one of the best in the world, you don’t want to live in SW15 if all of your friends live in N19.

And just as a final note, we discovered that properties with 3+ bedrooms tend to be unfurnished. We thought we would easily find a furnished house and only ship over our personal items but this does not seem to be the case. So either be prepared to ship over your furniture, or buy when you get there.

We settled on a lovely 3 bedroom house in Wandsworth, close to Wandsworth Town overland station, and within budget! We move in late November. I haven’t lived in a rental for over 7 years so that will be a bit weird again!