Comparison rates show that the cost of a loan is greater than just the interest rate.

I used to think the comparison rate shown by a financial provider was the highest rate with a competing financial provider for the same loan terms, to show how good their rate was. Comparison rates are actually a regulatory requirement for financial providers to supply. So they are not some dodgy rate used to mislead consumers. They actually have a good purpose.

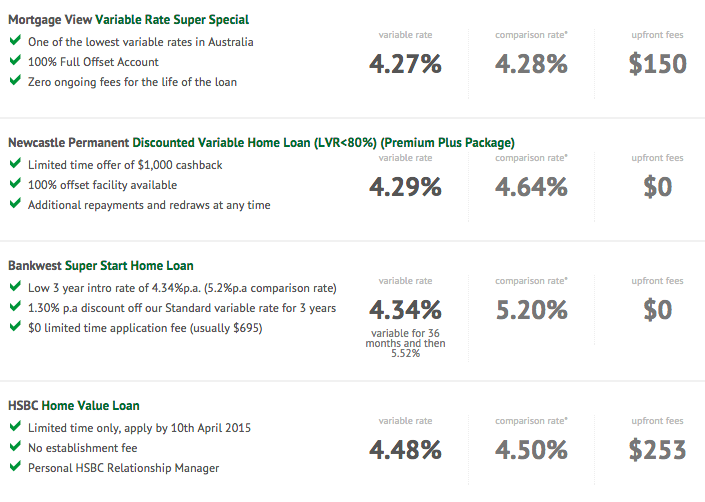

A comparison rate is used for any type of loan; home, car, personal etc, and is a combination of the annual interest rate and the equivalent in fees and charges, taking into consideration the amount borrowed, loan term and the repayment frequency, expressed in a total annual interest rate.

For instance, a $100k loan fixed for 3 years at 4.84% p.a, paying monthly, with a loan term of 25 years may incur fees and charges such as a $600 establishment fee, and a $10 monthly service charge. The interest rate and the equivalent of all of these fees gives a comparison rate of 5.51% p.a.

Basically the 5.51% is comprised of:

- The annual interest rate of 4.84% for three years, and then a proxy rate for the remaining 22 years of the loan, plus

- The one off establishment fee of $600, incurred at the start of the loan, plus

- The $10 monthly service fees, over the 25 year term of the loan, which is 300 payments totalling $3,000, calculated in present value.

Note that there can be many other fees incurred on a loan that are not included in the comparison rate. These fees are not known because they may or may not be incurred, and some examples are: redraw fees, late payment fees, and early repayment fees. Comparison rates also do not include other purchasing fees such as stamp duty, solicitors costs and mortgage registration fees.

The fundamental premise behind comparison rates is sound – it is trying to represent to consumers that the cost of a loan is greater than just the interest rate and quantifying this in an easily comparable way via an “all-in-rate”. The National Credit Code (NCC) enforces comparison rates and “requires that credit providers include a comparison rate when they advertise fixed term credit which is for, or mainly for, personal domestic or household purposes.”

However the problem with comparison rates is that there are so many inputs into the calculation that they are actually very difficult to… compare. When reviewing comparison rate quotes there will always be a footnote, which you should read. It could say something like this “This comparison rate is based on a secured loan of $150,000 over the term of 25 years. WARNING: The comparison rate applies only to the example given…. Different amounts and terms will result in different comparison rates….” So if you’re looking at borrowing anything other than $150k, for instance, the comparison rate will not be useful. And different lenders can calculate their comparison rate on different loan conditions.

I would suggest speaking to a mortgage broker who can do the leg work for you and find some of the best rates for your situation, understand the different types of fees for each product, and present all of the options to you in a clear way. As always, check how the broker is remunerated to ensure you’re not being sold products they receive more commission on than others.